|

Budgeting & Manpower Planning:Top-down or Bottom-up?

With the end of the third quarter around the corner, it marks the time of the year for HR leaders to partner with Finance counterparts to drive the annual budget and manpower planning process. A strategic HR leader would embrace these processes to gain credibility from the executive team – a great opportunity to reposition and reinforce HR as a strategic partner. However, as most of the HR leaders are not finance experts and the budget process could be daunting, some of them may just abdicate their responsibilities and leave this strategic task to their Finance counterparts. Some HR leaders face difficulties in collecting relevant data for the budget process while others may have issues with knowing what data needs to be collected and where to start. Budgeting involves the systematic collection of both historical actual data and forward looking business forecast so as to achieve firm’s short and long-term objectives. A widely adopted approach of budgeting involves using the current numbers to make upward or downward adjustments to each item based upon expectations. In most companies, staff costs make up the majority of fixed costs, HR typically collects the following information for budgeting purposes:

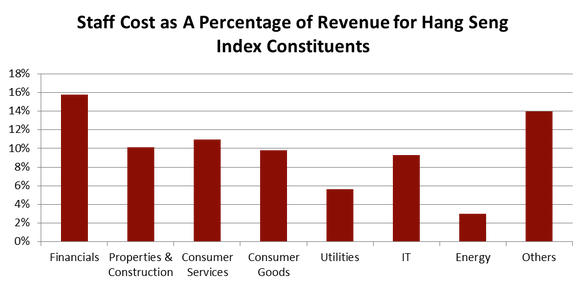

Bottom-up: Projecting Current Staff Costs is Not Always Easy… After collecting the above data, the easiest way out is to adopt a bottom-up approach by projecting current compensation costs incrementally and use that as the base by adding the new headcount and subtracting the number by the projected attrition. This seemingly logical approach has actually oversimplified the calculation as it assumes current pay levels are largely competitive and a broad-brush year-over-year salary movement is usually applied across all employees. In addition, the long-term business perspective may not be fully considered by this approach. A more holistic bottom-up approach is to benchmark individual employees against market pay levels as the starting point for budget planning and identify the specific functions, positions or levels that are under competitive pressures. Then HR leaders needs to identify the pay gap and customize the necessary salary movement that is needed for retention purpose to determine the necessary compensation budget. The incremental bottom-up budget and manpower plan is rather simple and easy to put into practice. However, it is more suitable for firms with stable year-over-year growth which allows for gradual change within the company. As stability is the keyword here, it does not account for major business expansion or downturn since substantial variance to previous year’s budget is being frowned upon. In reality, HR leaders often find significant deviations between actual and budgeted costs due to major changes in operations and business environment along the year. This rather simple bottom-up budgeting process is insufficient to cope with these fundamental changes and it often encourages a detrimental “use it or lose it" mentality among business heads when business outlook cannot justify the planned staff costs and headcount. An Alternative Approach: Top-down As opposed to the incremental bottom-up budgeting, a top-down perspective provides an alternative to provide a logical yardstick. As compensation and benefits costs made up a big chunk of the total costs, an initial compensation budget could be developed based on the benchmarking outcome of compensation and benefits costs as a percentage of revenue against target comparator groups. This will provide a high-level reference on the market range of compensation expenses to start with and offer an overall perspective on whether the total compensation costs is justified. |

Using Key Metrics to Break Down the Numbers

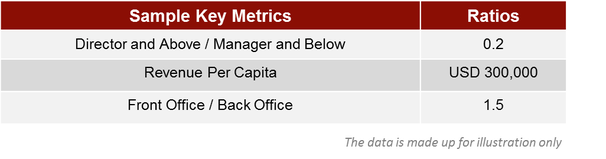

After getting the total compensation and benefits budget right, the total costs can then be translated and broken down into headcount numbers by referencing appropriate staff mix in the market. For instance, company scale like market capitalization and revenue size could be one of the key drivers for a company to determine the staff mix. By benchmarking some key metrics against the target comparator group based on company scale, this will provide a relevant reference on how to best structure the manpower plan and to come up with the corresponding budget. Typical ratios to consider include:

After getting the total compensation and benefits budget right, the total costs can then be translated and broken down into headcount numbers by referencing appropriate staff mix in the market. For instance, company scale like market capitalization and revenue size could be one of the key drivers for a company to determine the staff mix. By benchmarking some key metrics against the target comparator group based on company scale, this will provide a relevant reference on how to best structure the manpower plan and to come up with the corresponding budget. Typical ratios to consider include:

The role of HR is therefore to provide the overall compensation and benefits budget as well as guidance on the application of the above key ratios to facilitate the budget and manpower planning process. This is then expanded by each department to form a detailed budget. Reference could be made to zero-based budgeting approach which requires the justification for incurred expenses. Instead of starting off with last period's budget, every business unit has to go through and justify every expense that will incur during the course of business and be held accountable for the necessary expenses. This incudes the explanation of how the projected costs will contribute to the target revenue or profit generation.

Each firm should consider their business nature, company scale (such as revenue, market capitalization, geographic coverage, etc.), and development stages to structure the proposed staff mix and budget for the new year. For a more detailed breakdown of the manpower and budget plan (including headcount by grade), reference could also be made to ratios such as employee distribution among different back office functions, employee distribution across various grades among target comparator group, etc. This will provide another perspective to review the firm’s own employee distribution ratio and how the new manpower plan and budget should be adjusted accordingly.

Putting it Together: A Combined Approach

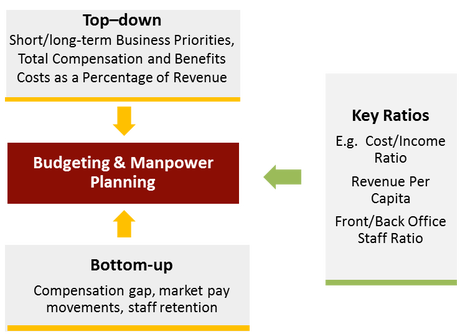

No matter which approach a company adopts, it has its own merits and demerits. In practice, more companies go for a combined approach with both top-down and bottom-up budget processes which can address most of the downside of just applying one approach. Reconciling the top-down numbers with the outcome of the bottom-up gap analyses between current pay levels and market competitive levels will provide a good source of reference to assess and justify whether the proposed budget is reasonable. These numbers would then be cross checked with the various key metrics and ratios to ensure that the proposed budget and manpower plan is within a reasonable range to support the business requirements.

Each firm should consider their business nature, company scale (such as revenue, market capitalization, geographic coverage, etc.), and development stages to structure the proposed staff mix and budget for the new year. For a more detailed breakdown of the manpower and budget plan (including headcount by grade), reference could also be made to ratios such as employee distribution among different back office functions, employee distribution across various grades among target comparator group, etc. This will provide another perspective to review the firm’s own employee distribution ratio and how the new manpower plan and budget should be adjusted accordingly.

Putting it Together: A Combined Approach

No matter which approach a company adopts, it has its own merits and demerits. In practice, more companies go for a combined approach with both top-down and bottom-up budget processes which can address most of the downside of just applying one approach. Reconciling the top-down numbers with the outcome of the bottom-up gap analyses between current pay levels and market competitive levels will provide a good source of reference to assess and justify whether the proposed budget is reasonable. These numbers would then be cross checked with the various key metrics and ratios to ensure that the proposed budget and manpower plan is within a reasonable range to support the business requirements.

While the combined approach might seem more complicated to manage, it means the company will be in a better position to reap the benefits of the combined approaches and mitigate the common flaws of individual approach. When supported with well-defined manpower planning and budgeting processes, this combined approach is effective in linking the budget of all levels of the firm to the wider company strategies. This put HR at the center of the executive table to promote a level of confidence and buy-in that makes the business objectives more achievable.