|

Differentiating Bonus with Performance

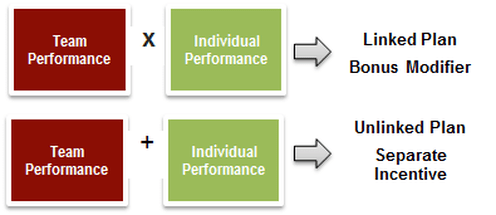

Pay-for-performance has become part of the organization culture for many leading companies. It is the motto that drives compensation philosophy, incentive design and performance management programs. Companies have come to realize the devil is in the implementation details. Some of them only pay lip service as they adopt a broad brush approach in paying bonus. Others simply apply whatever the market dictates which has led to insufficient pay differentiation. Pay-for-performance can sometimes seem an illusory concept as it can have very different meanings to different employees within the company. CEOs often face the dilemma on how to balance different levels and aspects of performance and to what extent the defined performance combine with other considerations in determining bonus payouts. Differentiate from the Top As oppose to just benchmarking and applying the overall bonus payout ratio to determine the firm wide bonus pool, companies have to consider both external factors such as macro business performance and internal factors such as company profit to reinforce pay-for-performance. Bonus payout ratios have to be differentiated across companies based on scale of the business, development stage and firm-wide performance and current pay competitiveness to prevent potential windfall or shortfall in bonus payout. Multiple Levels of Performance and their Relationship Apart from company performance, performance can also include departmental / team and individual performance. For companies that adopt target bonus approach, an important question is whether the different levels of performance are linked or separated when determining the bonus equation. When team performance and individual performance are multiplied, it shows incentive is determined by achievement of team’s KPIs and final payout is modified by individual performance ratings or results. This encourages employees to strive their best in maximizing both team and individual performance. In order to operate a linked and multi-level bonus plan, the company can design KPIs and set targets for individual employees alongside team based KPIs. Nonetheless, this equation can be a double edge sword as it has both the advantage and disadvantage of magnifying the effect of team and individual performance in defining the final bonus payout. If the team underperforms and does not even meet the threshold requirement, bonus intended for individual performance will be wiped out altogether. If the two levels of performance are added up instead, it means the two performance elements are unlinked in the equation. Bonus is the sum of separate awards for achievement of team’s objectives and individual performance. This gives rise to the need to assign weightings to reflect the relative importance of different levels of performance. It is often an art rather than science to strike a balance as the relative weightings can vary based on the extent of company franchise, nature of business/functions and governance model. The addition approach provides a safeguard that employees will, to a large extent; get some bonus as a result of team or individual performance. This could be good news to employees when compared to the multiplication approach. Which bonus approach works better will be highly dependent on the kind of behavior that executives want to drive and to what extent bonus fluctuates according to performance at different levels.

Balancing Quantitative versus Qualitative Performance No matter one is referring to company, departmental / team and individual performance, all of them consist of both quantitative and qualitative aspects. For KPIs such as profit or revenue that are more financial and quantitative in nature, performance assessment is largely based on achievement of the preset targets. Pay-for-performance can sometimes lead to unintended behavioral consequences and might unnecessarily encourage short-term behaviors and/or excessive risk taking as exemplified in the Wells Fargo case. Thus, financial KPIs should not be the sole performance criteria in determining the overall bonus pool. Some qualitative and more long-term goals, such as product and channel development, strategic collaboration or expansion, have to be incorporated to enable long-term growth. Nonetheless, the last thing that company wants is a myriad of KPIs that are not only costly to measure but also diverts attention on the key result areas. Some companies deploy a balanced scorecard framework to strike a balance between different aspects of financial and non-financial KPIs in measuring firm-wide and departmental performance. Some companies just benchmark and determine the average number of monthly salaries to be paid to each department. It is better to determine or allocate the firm-wide pool to department level according to its degree in fulfilling the KPIs. To ensure bonus is sufficiently differentiated and allocated, other factors such as change in team performance, projected bonus movement and bonus requirements for maintaining competitive pay levels have to be taken into considerations. If we zoom into individual performance, there are even more factors to consider during the appraisal process. All the way, we have been emphasizing the importance of both process and results in measuring individual performance. Apart from measuring performance against achievement of objectives, the process on how the objectives are met is also rated through competency assessment.

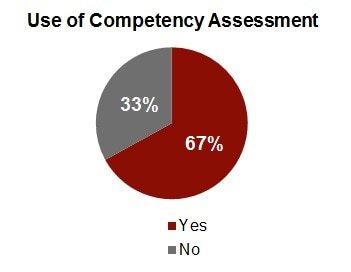

The pie chart above indicates two-third of the benchmarked companies include competency assessment as part of the performance review process while other companies conduct competency assessment only for employee developmental purpose. Actually, results from competency assessment, e.g. teamwork, communication, initiative, etc. can also be incorporated in the bonus formula to reflect the qualitative aspects of performance. How quantitative and qualitative KPIs as well as competency ratings are combined to measure performance highly dependent on the extent of control or influence that the employees can exert on those components. Similarly, whether the company is in favor of using a multiplication or addition approach in the bonus equation depends on the prevailing organization culture and the degree of bonus volatility tolerated.

For companies which include competency assessment as part of the appraisal process, objective assessment has always been challenging. Some of them have come up with different assessment approach conducted by multiple raters in a bid to minimize bias during the process. The more sizable companies typically provide performance distribution guidelines to department heads to prevent over-rating by conforming to a normal bell-curve. In reality, a skewed performance distribution is often found as department heads have a hard time to play the bad corps and avoid over-rating. A normal bell curve is almost impossible to implement especially when there are only a few employees in some departments to differentiate the good from the bad ones. These companies responded by conducting rounds of performance calibration meetings after initial performance ratings are assigned to review and justify performance ratings across employees at similar level. This can prevent bias and ensure differentiation as HR and/or senior management usually facilitates these calibration meetings to ensure robustness and balance. Widen Performance and Bonus Differentiation After different levels and aspects of performance is determined, how these will affect the bonus payout can seem like a “black box”. For companies that prefer a target bonus or more formulaic incentive mechanism, the key considerations include:

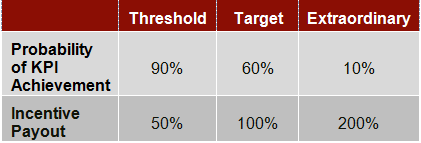

extent of performance and pay differentiation. Threshold means the minimum performance level that warrants incentive payment and typically with a 90% chance in achieving such target. As employees can achieve this even without much effort, usually only a minimal, for instance, 50% of the target incentive is paid. Target performance should be sufficiently stretched and challenging with around 60% chance in achieving the target. Extraordinary level refers to outstanding performance that only has around 10% probability in achieving it, thus warrants an exceptional payout at, for example, 2 times of the target incentive.

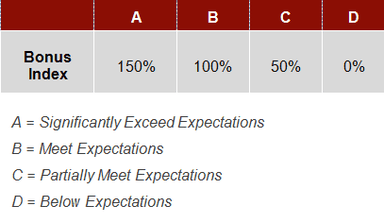

payroll ratios. The narrow difference in bonus allocation at individual level is not conducive to pay for performance and differentiation. To maximize differentiation, every department head should keep track of employee performance throughout the year based on their goal achievement, competency levels, contribution, etc. Employees’ performance is differentiated and classified into 4 to 5 tiers as illustration on the table below. Bonus payout will then reflect such differentiation by assigning different bonus index during the allocation. The total pool is allocated through dividing each individual’s bonus index by the sum of all indexes. The resulting percentage determines each individual's share of the pool.

Regardless of one is adopting a more formulaic or discretionary approaches in linking pay with performance, the key is to ensure all rounded perspectives to performance and widen the differentiation. A dynamic and holistic approach is necessary by combining performance with market data and forecast to balance all the conflicting forces behind the pay and performance decisions to ensure the company can really live and breathe the performance oriented culture.

Case Study: Using Discretion to Widen Differentiation

A listed company (“XYZ”) with multiple businesses is preparing pay review and bonus proposal for its Deputy Chief Executive Officer (“DCEO”) who is in charge of a major business. It has been using a discretionary bonus approach in determining bonus. The key facts are:

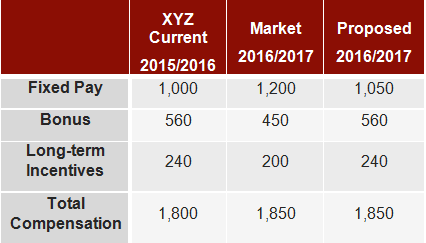

The table below shows the current and market compensation levels for XYZ. The market data is projected based on latest market forecast on salary and bonus movement. (Due to confidentiality, data is made up for illustration purpose)

The proposed pay levels are based on the rationale that the firm-wide bonus pool has dropped by 10% due to a decrease in overall profit. However, total incentives (i.e. bonus plus long-term incentives) will remain unchanged to reflect departmental performance is still showing signs of growth and reward exceptional individual performance despite a more volatile market conditions and increasing regulatory influence. This recommendation balances the need to share the burden for the company’s downturn and the need to differentiate and reward outstanding team and individual performance.

Although the projected inflation rate for 2017 is 2.6% and the projected salary increase median is 4.3% respectively, fixed pay remain largely flat for senior management in the market. In view of current competitiveness of fixed pay and total compensation, the monthly salary for the DCEO is recommended to increase to HK$1,050 to catch up with the market. |

Related Links

Should you want to obtain more information, please contact us by [email protected] or call us at +852 3996 7868 |

|

|

- Home

-

What's New ?

- Bonus Pick Up Partially Offset Slower Pay Increase in 2024

- 1 x 1 = >10? Combine Talent Pass with Long-term Incentives to Maximize Talent Pool

- Dual Impact of Bonus Plunge and Great Resignation Drive Staff Turnover to 5-Year High

- Pay will be Above Pre-COVID levels; Financial Industry is Ahead in Benefiting from Recovery

- Incentive Pay Makes Top US CEOs and CFOs Best Paid in World, According to First-Ever Global 250 Survey

- How to Retain Key Talent after Bonus Season?

- Differentiating Bonus with Performance

- Is a Formula Better than Discretion in Paying Incentives?

- Rippling Effect – More Industries Embrace Partnership

- Globalization – It’s Easier Said Than Done

- Strengthen Performance Planning to Drive Performance Management

- Benefits as Essential Tool for Improving Employee Engagement

- Shifting Away From “Low Pay, High Bonus” for Sustainability

- Strengthen Pay & Performance Alignment For Top Executives

- Budgeting & Manpower Planning: Top-down or Bottom-up?

- Maximizing Employee Benefits

-

Challenges & Solutions

-

Research & Events

- Pretium Pay & Performance Survey

- Pretium Compensation Level Survey

- Pretium Incentive Practices Survey

- Pretium Staff Ratios and Manpower Budgeting Survey

- Pretium Benefits & Employment Conditions Survey

- Pretium Year-end Rewards & HR Trends Survey >

- Independent Non Executive Director Fee Study

- Long-Term Incentive Survey Report – General Industries

- Global Top 250 Compensation Survey Report

- Retail Brokerage Survey

-

Case Studies

- Develop Performance Aligned Salary Structure

- Review Pay Positioning to Steer Growth

- Incentivize and Retain Senior Executives to Drive Performance

- Promote Partnership with Long-term Incentives

- Pre-IPO Long-Term Incentive Design for a Diversified Company

- Strengthening Short-Term Incentive Strategy

- Carried Interest and Performance Management

- Strategic Compensation and Benefits Advisory Services

- One-stop Human Resources Solutions

- Grading and Job Title System

- Career

- 中文